How to Get Preapproved for a Mortgage in Portland, Oregon 2026

How to Get Preapproved for a Mortgage in Portland, Oregon 2026

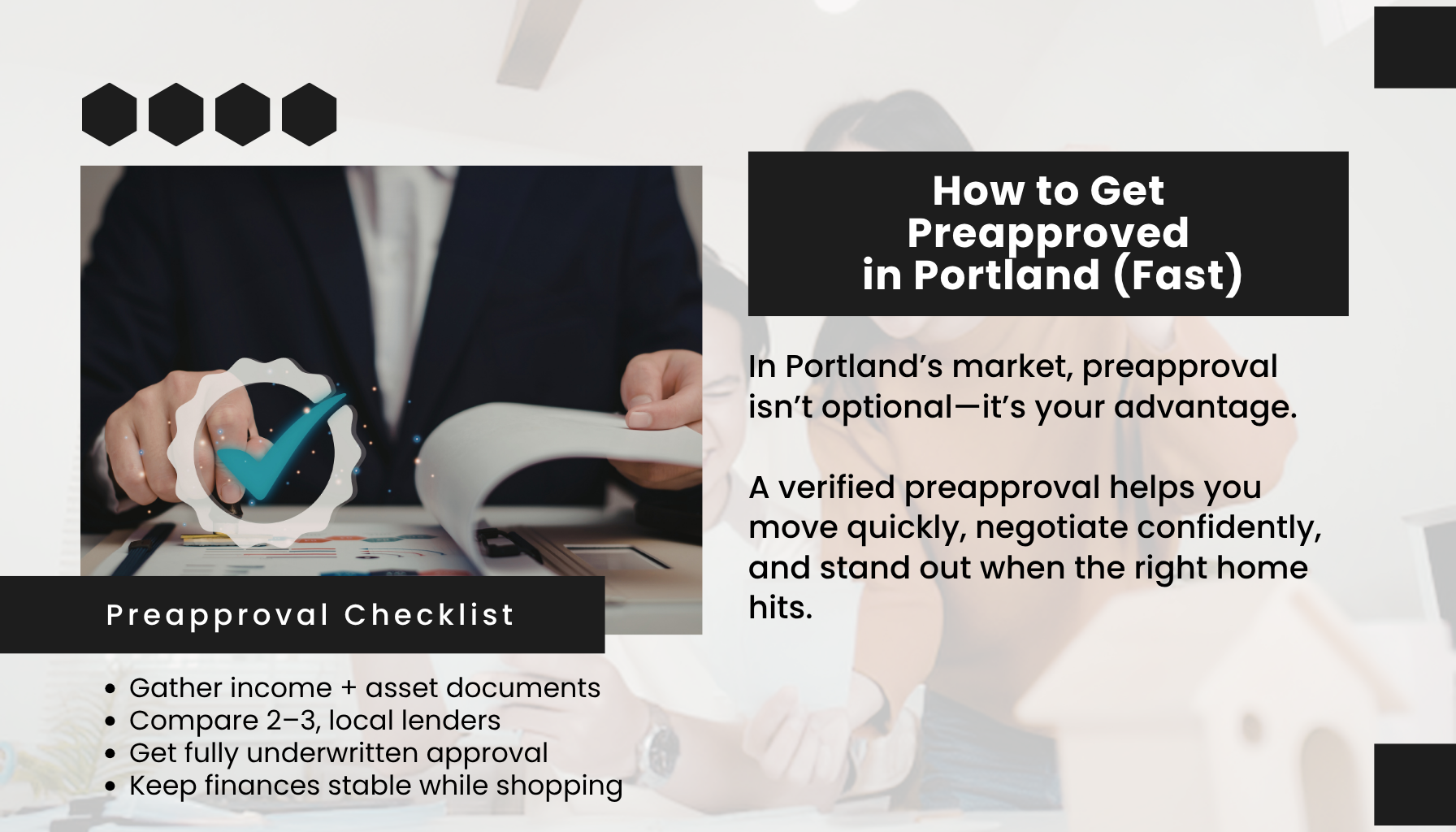

How do I get preapproved for a mortgage to buy in Portland Oregon

The fastest path to preapproval in Portland, Oregon is to gather your documents, compare 2-3 local lenders, and complete a full credit and income review so you receive a verified letter you can use to write confident offers within days.

Why Mortgage Preapproval Matters Right Now in Portland, Oregon

You’re shopping in a market that is tilting in your favor, but you still need proof you can close. Portland’s average home value sits around 524,251, with the median sale price near 507,333 and a median list price near 499,600. Inventory reached roughly 1,968 homes in February 2026, and 51.7% of sales closed under list price. At the same time, 27.2% still sold over asking, and the median days to pending is about 33 days. That mix means you can negotiate, but you must also act decisively when a great home hits. A strong preapproval helps you beat hesitation, move quickly, and signal to sellers that you’re serious. With price reductions near 23.3% in January and days on market at 95 for that month, you have time to evaluate options, but the best listings still draw attention. Getting preapproved now puts you in position to lock in a home at a fair price while inventory remains favorable.

What You Need to Know Before Getting Preapproved in Portland

You should align your budget with Portland pricing and your long-term comfort. Prices have moderated slightly year over year and are roughly 20% above 2020 levels, so a precise budget matters.

Key points to prepare:

- Credit profile: Most lenders look for 620+ on conventional loans. FHA often allows lower scores. Better credit usually means better pricing.

- Debt-to-income ratio: Many lenders target 36% to 45% of your gross monthly income, including your new mortgage payment.

- Down payment: Options range from 0% for eligible VA buyers to 3% to 5% for many first-time conventional loans and 3.5% for FHA. Larger down payments can lower your rate and mortgage insurance.

- Cash to close: Plan for down payment, closing costs, and reserves. Closing costs typically include lender fees, third-party fees, taxes, and prepaid items.

- Income documents: Two years of W-2s, recent pay stubs, and full tax returns if self-employed. Expect verification of employment.

- Assets: Two months of bank statements. Keep funds seasoned and avoid large unexplained deposits.

- Assistance: Oregon Housing and Community Services periodically offers down payment and first-time buyer programs. Ask lenders which programs they can originate.

Preapproval vs prequalification in Portland

A true preapproval verifies income, assets, credit, and debt through underwriting. A prequalification is an estimate based on unverified info. Sellers in Portland will value a verified preapproval far more, especially in segments that still receive multiple offers.

How to Compare Lenders and Loan Options in Portland, Oregon

You will see differences in pricing, speed, and underwriting approach. Compare banks, credit unions, and independent mortgage lenders. Ask each for a written cost breakdown so you can compare apples to apples. Consider Portland’s 33-day median to pending timeline and choose a lender that can fully underwrite quickly and issue a strong letter.

Loan types to weigh:

- Conventional: Often best with stronger credit and 3% to 20% down.

- FHA: Flexible on credit and down payment, but includes mortgage insurance.

- VA: For eligible service members and veterans, often 0% down and competitive terms.

- ARMs vs fixed: Fixed rates bring stability. ARMs can lower initial payments, which might help if you plan a shorter hold.

Evaluate lender responsiveness during preapproval. Quick turn times matter when the right home appears. Also ask about local appraisal coverage and whether they can pre-underwrite your file. With 51.7% of Portland sales closing below list, you can negotiate, but a clean, fast close is often what secures a win.

Key factors to evaluate:

- Total APR and all lender fees, not just the rate

- Turn time to full underwriting and appraisal readiness

- Strength and specificity of the preapproval letter for Portland listings

Your Step-by-Step Mortgage Preapproval Guide for Portland Buyers

1) Set your target payment: Decide what you want to spend monthly, including taxes, insurance, and HOA dues if applicable. 2) Check credit early: Pull your credit report, correct errors, and pay down revolving balances to reduce utilization. 3) Gather documents: Two years of W-2s and tax returns if needed, 30 days of pay stubs, two months of bank statements, ID, and residency history. 4) Identify down payment sources: Personal savings, gifts with a gift letter, retirement account loans, or assistance programs. 5) Interview 2-3 lenders: Ask for scenario quotes at the same time of day and on the same day for fair comparisons. 6) Complete applications: Provide consent for credit pulls and upload documents promptly. 7) Underwriting review: Respond quickly to conditions. Ask for a credit and income verified preapproval, not just a prequalification. 8) Get a property-specific letter: Have your lender tailor each letter to the price range you plan to offer. 9) Keep your file warm: Preapprovals often expire in 60 to 90 days. Update pay stubs and statements as needed. 10) Protect your approval: Avoid new debts, large cash deposits, or job changes without discussing with your lender first.

What Mortgage Preapproval Looks Like in Portland, Oregon in 2026

Your budget needs to match Portland’s pricing bands. With a median sale price near 507,333, many first-time buyers target homes below the citywide median, where the median list price near 499,600 suggests entry points exist. Neighborhood differences are real. Recent neighborhood data shows Goose Hollow around 285,000 with longer average days on market near 112, which can give you leverage. Hillsdale sits higher around 765,000 with faster pace, and Collins View near 715,000. That spread means your lender letter should match the neighborhoods you’re targeting.

Because 51.7% of sales close under list and the median sale-to-list ratio is about 0.994, you can negotiate on many homes. Yet about 27.2% still sell over asking, especially well-priced homes in move-in condition. With 33 days to pending on median, you have a window to tour, revisit, and refine your offer. A verified preapproval lets you reduce contingencies responsibly, ask for seller credits in softer segments, and still move fast when a standout property appears.

What Most Portland First-Time Buyers Get Wrong About Preapproval

- Waiting to start: You lose weeks while others submit offers. Start preapproval before serious touring.

- Assuming the max is your budget: A lender’s maximum is not your comfort zone. Anchor to your target payment.

- Ignoring HOA dues and taxes: These swing qualifying power and monthly cost. Build them into your estimate.

- Shopping one quote: Pricing and fees vary widely. Compare at least two lenders on the same day.

- Moving money late: Large unexplained deposits create delays. Keep funds seasoned and documented.

- Thinking letters last forever: Most expire in 60 to 90 days. Update documents as you shop in Portland’s market.

Frequently Asked Questions

How long does mortgage preapproval take in Portland, Oregon?

You can often receive a preapproval in 24 to 72 hours once your documents are in. If your file is complex or self-employed, expect a few extra days. Ask for a credit and income verified letter so sellers view your offer as ready to close.

What credit score do you need to buy in Portland, Oregon?

Many conventional loans prefer 620 or higher, while FHA programs often allow lower scores with additional requirements. Higher scores can reduce your rate and mortgage insurance. Improve your score by lowering balances, disputing errors, and avoiding new credit.

How long is a preapproval letter valid in Portland?

Most letters are valid for 60 to 90 days. Keep pay stubs and bank statements current so your lender can refresh quickly. If rates or your finances change, your lender may need to update the letter before you write an offer.

Does preapproval affect your credit score in Portland, Oregon?

Yes, preapproval requires a hard inquiry, which may slightly reduce your score. Rate shopping with multiple lenders within a short window is usually treated as one inquiry for scoring purposes. The small impact is typically worth the benefit of stronger offers.

Should you use a local Portland lender?

You benefit from a lender who knows Portland taxes, HOA structures, and appraisal trends. Local lenders may underwrite and close faster, which helps in segments that still see multiple offers. Always compare speed, fees, and communication style.

What documents do you need for Portland mortgage preapproval?

Plan on two years of W-2s and tax returns if self-employed, 30 days of pay stubs, two months of bank statements, government ID, and your residence and employment history. Provide documentation for gifts, student loans, or other significant obligations.

Can you get preapproved with student loans in Portland?

Yes. Lenders count your student loan payment in your debt-to-income ratio. If your payment is income-based, they typically use the documented monthly amount. Bring your statements and repayment plan so underwriting can calculate your qualifying ratios accurately.

Is down payment assistance available in Portland, Oregon?

Yes. Oregon Housing and Community Services and local partners periodically offer down payment and first-time buyer programs, subject to income and purchase price limits. Ask lenders which programs they support and how assistance affects underwriting and timelines.

Are condos easier to qualify for in Goose Hollow?

Condos can be great entry points in Goose Hollow due to lower prices, but lenders also review the building’s budget, insurance, and owner-occupancy. Your preapproval should consider HOA dues and any special assessments that impact your monthly payment.

How many lenders should you compare in Portland?

Compare at least two, ideally three. Request quotes the same day with the same parameters so you can evaluate APR, fees, and estimated turn times. Choose the lender that pairs competitive pricing with clear communication and reliable local execution.

The Bottom Line

You get preapproved in Portland, Oregon by preparing your documents, aligning on a realistic payment, and securing a verified letter from a responsive lender who can move at the market’s pace. With inventory up, prices moderating, and 51.7% of sales closing under list, you have room to negotiate. Yet about 27.2% of homes still sell over asking, so you must be ready to act. A strong preapproval improves your offer terms, shortens timelines, and increases your confidence when the right home appears.

If you're ready to explore your options for mortgage preapproval in Portland, Oregon, Lisa Mehlhoff at Lisa Mehlhof Homes can walk you through the specifics for your situation.

503-490-4888

503-490-4888

Categories

Recent Posts

"My job is to find and attract mastery-based agents to the office, protect the culture, and make sure everyone is happy! "