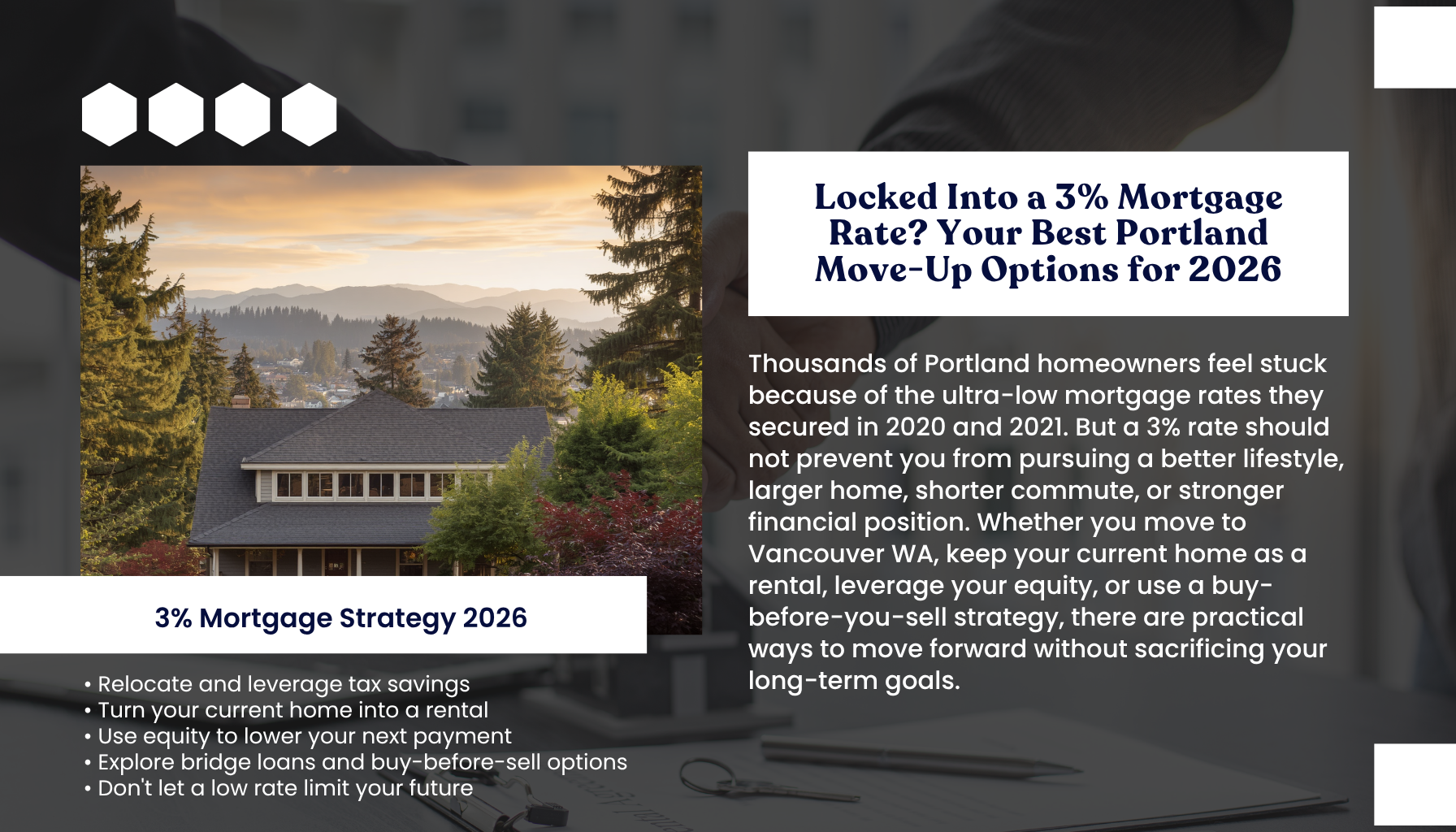

Real Options for Portland Oregon Homeowners Locked Into a 3% Mortgage Rate

If you locked in a 3% mortgage rate during 2020 or 2021 but your life has outgrown your home, what are your real options in the Portland metro market right now?

[SNIPPET ANSWER: Portland homeowners with low rates can offset higher costs by leveraging equity, relocating to no-income-tax Washington, using buy-before-you-sell strategies, or renting out their current home as an investment.]

Why This Matters for Portland Oregon Homeowners Right Now

Here is the reality. You bought your home in Northeast Portland or Sellwood at 2.75% or 3.25%, and the thought of trading that rate for something near 6.5% to 7.0% feels like setting money on fire. You are not alone. Across Portland Oregon real estate, this exact dilemma has frozen thousands of homeowners in place for the past three years.

But something shifted in early 2026. New listings in the Portland metro and Southwest Washington real estate markets surged. Pending sales jumped nearly 48% in Clark County alone. The "wait and see" era is ending because life does not wait for interest rates. Your family grew. Your commute changed. Your kids started school in a different district. Your job relocated.

With 20 years of experience helping buyers and sellers navigate exactly these crossroads, I can tell you that the homeowners who move strategically in this market come out ahead. The ones who stay paralyzed by a number on paper often miss their window. Let me walk you through every viable path forward.

The Real Cost of Keeping Your 3% Rate in Portland Oregon

Before you decide to stay put forever, let's do some honest math. That 3% rate is only valuable if the home still fits your life.

Consider what staying actually costs you:

- Opportunity cost on equity. Portland median home prices sit near $545,000. If you purchased in 2020 at $425,000, you may be sitting on $120,000 or more in equity that is doing nothing for you while you sleep in a house that no longer works.

- Career limitations. If a higher-paying position opened up in Vancouver WA or Battle Ground Washington, staying locked to your Portland mortgage means potentially leaving $15,000 or more in annual income tax savings on the table.

- Quality of life costs. The extra bedroom, the shorter commute, the better school district, the yard your kids need. These have real, measurable value that a spreadsheet cannot always capture.

One couple I worked with in the Alberta Arts District had a beautiful bungalow at 2.875%. They also had three kids sharing two bedrooms and a 45-minute commute to a new job in Vancouver. When we calculated the Washington state income tax savings against the higher mortgage payment, their net monthly cost actually dropped by relocating to Battle Ground Washington. They could not believe the numbers until we walked through every line together.

So what are the actual strategies? Let me break them down.

Option 1: Relocate to Vancouver WA or Clark County and Pocket the Tax Savings

This is the single most powerful financial lever available to Portland Oregon homeowners right now, and it is one I discuss with clients almost every week.

Washington has no personal state income tax. If your household earns $200,000 per year, relocating from Multnomah County to Clark County can put more than $15,000 back into your pocket annually. Over a 30-year mortgage, that is $450,000 in tax savings alone, before accounting for investment growth.

What the Numbers Look Like in Vancouver WA

The median sale price in Vancouver sits at $489,000, with homes selling in roughly 18 days. Homes priced between $425,000 and $500,000 move fastest. Compare that to Portland's $545,000 median, and you are looking at a lower purchase price combined with massive tax savings.

Here is what this looks like in practice:

- Your current Portland home: $540,000 value, 3% rate, $2,275 monthly payment (principal and interest)

- New Vancouver WA home: $490,000, 6.5% rate, roughly $3,100 monthly payment

- Monthly increase: About $825

- Monthly income tax savings: About $1,250 or more for a $200,000 household

The net result? You are actually ahead each month, living in a home that fits your life, in a market that was ranked the seventh healthiest real estate market in the nation.

Option 2: Keep Your Portland Home as a Rental and Buy Your Next Home

If your Portland property sits in a high-demand rental corridor like Laurelhurst, Irvington, Woodstock, or Foster-Powell, keeping it can be a wealth-building play. Your 3% rate becomes an asset on the investment side because your carrying costs are dramatically lower than what a new investor would face.

How This Strategy Works in Portland Oregon Real Estate

- You keep the 3% mortgage on your current home

- Rental income in desirable Portland neighborhoods can cover most or all of your existing mortgage payment

- You purchase your next home at current rates, using equity from a HELOC or savings for the down payment

- Over time, you build equity in two properties while your tenant pays down your original mortgage

This approach works especially well for tech professionals and doctors relocating within the metro. A physician I helped last year kept her Sellwood condo while purchasing a larger home in Brush Prairie Washington, where the Hockinson School District offered exactly the smaller, community-focused environment she wanted for her kids. The condo rental income covered 90% of her old mortgage, and the Brush Prairie property gave her family the space and privacy they needed.

One important note: most properties in Brush Prairie rely on private well and septic systems rather than municipal utilities. This is standard for acreage properties there, but it is something you need to factor into your decision and budget for inspections accordingly.

Option 3: Sell, Deploy Equity, and Buy Down Your New Rate in Battle Ground Washington

If keeping two properties feels like too much complexity, selling your Portland home and using your equity aggressively on the next purchase is a clean, powerful option.

The Battle Ground Washington Opportunity

Battle Ground's median home price ranges from $495,000 to $580,000, and well-priced homes in the $500,000 to $700,000 range still attract multiple offers. The city has grown to approximately 24,000 residents, up roughly 15% since 2020, with strong schools in the Battle Ground School District serving over 12,700 students.

Here is where your equity becomes your rate:

- Sell your Portland home and net $150,000 in equity after closing costs

- Put 30% to 40% down on a Battle Ground home instead of the minimum

- Your larger down payment means a smaller loan balance, so even at 6.5%, your monthly payment stays manageable

- Use remaining equity to buy down your rate with discount points, potentially getting to 5.75% or lower

When you combine a larger down payment, a rate buydown, and Washington's income tax advantage, the monthly picture gets surprisingly close to what you are paying now. Not identical, but close enough that the lifestyle upgrade makes it a clear win.

Option 4: Use a Bridge Loan or Buy-Before-You-Sell Strategy

One of the biggest fears I hear from homeowners across Portland Oregon real estate is this: "What if I sell my house and cannot find the next one in time?" It is a valid concern, especially with homes for sale in Portland Oregon and homes for sale in Vancouver WA moving in under 20 days.

A bridge loan lets you access equity in your current home to purchase your next property before listing. You move once, on your timeline, and then sell your vacated home, which typically shows better and sells faster when it is empty and professionally staged.

Having closed over 165 transactions across the Portland metro and Southwest Washington, I can tell you that the buy-before-you-sell approach has become increasingly popular in 2026. The emotional relief of knowing you have your next home secured before your current one hits the market is significant, especially for families with school-age children who need continuity.

Option 5: Explore Assumable Mortgages and Creative Financing in Portland

This option is less common but worth understanding. If you hold an FHA or VA loan at 3%, your mortgage may be assumable, meaning a qualified buyer can take over your exact loan terms. This makes your home dramatically more attractive to buyers and can often command a premium sale price.

For military families in the Portland metro, VA loan assumptions are particularly powerful. And if you are a veteran purchasing your next home, VA loans typically come with rates 0.25% to 0.5% lower than conventional options, with zero down payment and no PMI.

Frequently Asked Questions

Is it worth giving up a 3% mortgage rate to move in Portland Oregon?

It depends on your full financial picture. When you factor in equity gains, potential tax savings from relocating to Washington state, and quality of life improvements, many homeowners come out ahead. The rate is only one piece of the equation, and I encourage every client to look at the complete picture before deciding.

How much can I save by moving from Portland to Vancouver WA?

A household earning $200,000 annually can save more than $15,000 per year in state income taxes by relocating to Clark County. Over a decade, that totals $150,000 or more in savings that can directly offset a higher mortgage rate.

What are homes selling for in Battle Ground Washington in 2026?

The median home price in Battle Ground ranges from $495,000 to $580,000. Well-priced properties in the $500,000 to $700,000 range continue to attract strong buyer interest, with new construction remaining active in areas like the Dollars Corner growth corridor.

Can I keep my Portland home as a rental if I move to Southwest Washington?

Yes, and this is one of the most effective strategies for preserving your 3% rate as an investment tool. Neighborhoods like Woodstock, Sellwood, and Irvington generate strong rental demand that can cover most or all of your current mortgage payment.

How long are homes taking to sell in Portland Oregon right now?

Portland homes are moving in approximately 19 days on average, with properties selling at about 100.56% of asking price. In Vancouver WA, the average sits at 18 days. This pace rewards sellers who are prepared and priced correctly.

What is the median home price in Brush Prairie Washington?

Median list prices in Brush Prairie start around $628,000 and up, with inventory spanning entry-level acreage to multi-million-dollar estate properties. The area's limited land supply and zoning constraints support strong long-term price stability.

Are VA loans a good option for buying in Portland or Vancouver WA in 2026?

VA loans remain one of the strongest tools available, offering zero down payment, no PMI, and rates typically 0.25% to 0.5% below conventional options. For military families transitioning or retiring to the Portland metro, this benefit can significantly reduce the sting of current rates.

What Portland neighborhoods are best for first-time buyers in 2026?

St. Johns in North Portland often offers single-family homes below the city median. Southeast neighborhoods like Foster-Powell and Lents also provide relative affordability with strong community character and access to local parks and businesses.

How do Oregon property taxes compare to Washington?

Oregon's Measure 50 limits annual assessed value increases to 3%, and Multnomah County's effective tax rate is approximately 1.02%. Washington has no state income tax but does have property taxes. The net benefit depends heavily on your income level and home value.

Should I wait for mortgage rates to drop before selling my Portland home?

Waiting carries risk. Portland home prices are expected to appreciate 3% to 4% in 2026, meaning the home you want to buy gets more expensive with each passing quarter. Pent-up demand is already driving early activity across the market, and competition for well-priced homes is increasing. Understanding current mortgage rates can help inform your timeline and financing strategy.

The Bottom Line for Portland Oregon Homeowners

Your 3% rate was a gift. But clinging to it while your life requires something different is not a financial strategy. It is avoidance. The Portland Oregon real estate market and Southwest Washington real estate markets both offer real, tangible paths forward, whether that means leveraging the Washington income tax advantage, turning your current home into a rental, deploying equity strategically, or using creative financing to bridge the gap.

Every situation is different, which is exactly why a Portland Oregon real estate agent with deep local knowledge matters. With 20 years of experience, 165 closed transactions, and 24 five-star reviews from clients who faced these exact decisions, I help homeowners see the full picture, not just the rate. If you are weighing your options, reach out to Lisa Mehlhoff at 503-490-4888. Let's look at your numbers together and find the move that actually makes sense for your life.

Categories

Recent Posts

"My job is to find and attract mastery-based agents to the office, protect the culture, and make sure everyone is happy! "