How much down payment do you need to buy in Portland Oregon in 2026

How much down payment do I need for a first time home in Portland Oregon 2026?

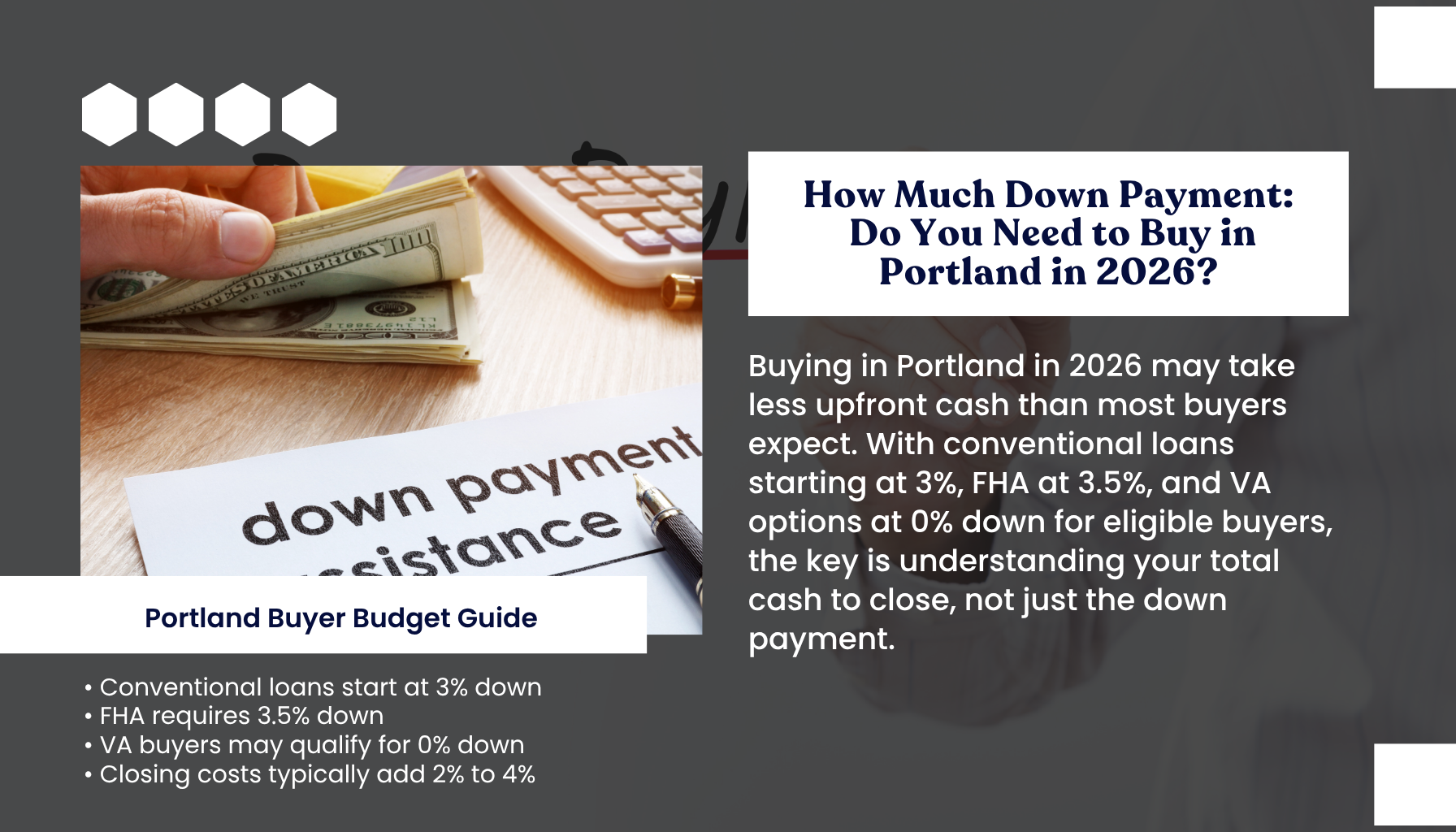

In Portland Oregon in 2026, you typically need 3% to 5% down on a conventional loan or 3.5% with FHA. On a $559,500 median-priced home, that’s about $17K to $28K for down payment plus roughly 2% to 4% for closing costs.

Why This Matters Right Now in Portland Oregon

You’re stepping into a resilient Portland housing market with more inventory and steady demand. According to recent market overviews, Portland’s median home price hovered around $559,500 in late 2025, days on market averaged 44, and inventory grew month over month. Pair that with interest rates near 6.5% in early 2026, and your upfront cash plan directly affects your monthly payment, buying power, and negotiation leverage. If you’re relocating for Intel, Nike, or OHSU, or you’re a first-time buyer, this is why this matters to you. With more homes to choose from, you can use credits, buydowns, and loan programs to reduce cash to close and secure a payment that fits your life. A clear, neighborhood specific plan helps you move confidently.What You Need to Know Before You Budget in Portland Oregon

You should decide on your loan type first because it sets your minimum down payment and impacts monthly costs.- Conventional: 3% minimum down for many first-time buyers. Private mortgage insurance applies until you reach 20% equity.

- FHA: 3.5% minimum down with flexible credit standards. Upfront and monthly mortgage insurance applies.

- VA: 0% down if eligible. No monthly mortgage insurance. A funding fee may apply.

- Jumbo: Typically 10% to 20% down for higher price points in areas like Laurelhurst or Irvington.

- Closing costs: Plan on 2% to 4% of the purchase price for title, escrow, lender fees, taxes, and prepaids in Oregon or Southwest Washington.

- Credits and grants: Seller credits, lender credits, and first-time buyer assistance can offset closing costs. Program rules, income limits, and county loan limits apply.

- Monthly impact: With rates near 6.5%, an extra 2% down can improve your payment or allow you to buy in a preferred area like Alameda Portland homes or Sellwood.

- Reserves: Keep 2 to 6 months of expenses after closing. That’s your safety net for ownership and is key to the C3 approach of care, confidence, and communication.

Quick math on a sample Portland purchase

Using Portland’s recent median of $559,500:- 3% down: about $16,785

- 3.5% down: about $19,583

- 5% down: about $27,975

- Closing costs 2% to 4%: about $11,190 to $22,380

- FHA upfront MIP is about 1.75% of the base loan and can be financed

How to Compare Your Down Payment Options in Portland Oregon

Your best option balances upfront cash, monthly affordability, and speed to homeownership.- If you want the lowest cash to close: VA is 0% down for eligible buyers. FHA at 3.5% is often the next lowest. Both allow gifts and some assistance programs.

- If you want lower monthly payments over time: Conventional at 5% or higher often lowers PMI cost and makes it easier to remove mortgage insurance later, especially in rising Portland property values.

- If you need to maximize approval: FHA is more forgiving on credit and debt-to-income. Good for first-time buyers ready to move now in areas like Foster Powell homes or Northeast Portland real estate.

- If you’re eyeing Portland luxury homes or Lake Oswego homes for sale: You may need 10% to 20% down to qualify for jumbo pricing or to meet stricter reserves.

- If you plan to house-hack or buy a condo vs house: Check condo warrantability and HOA dues. Lower down may work, but underwriting is tighter. Your payment can still be right if HOA plus PMI fits your target.

- If you’re considering moving to Southwest Washington: Vancouver WA homes for sale, Brush Prairie homes for sale, and Battle Ground Washington can offer price flexibility. Washington has no state income tax while Oregon has no sales tax. Compare your net take-home and closing cash carefully.

Key factors to evaluate:

- Total cash to close versus time to save and potential Portland market trends

- Monthly payment at today’s rate versus a potential buydown or larger down payment

- Property type, HOA dues, and condition, since repairs and fees change affordability

Your Step-by-Step Guide to Estimating Cash to Close in Portland Oregon

Follow these steps to build a clean number and stay in control.1) Get a full preapproval. Ask for side-by-side quotes for conventional 3% to 5%, FHA 3.5%, and VA if eligible. This is your apples-to-apples view. 2) Set your target price by neighborhood. Keep it neighborhood specific. Compare Southeast Portland real estate near Sellwood to Northeast options near Irvington or Alameda. 3) Choose your loan type. Pick the best balance of upfront cash, payment, and approval odds. 4) Calculate down payment. Multiply the price by your chosen percentage. On $559,500:

- 3% is about $16,785

- 3.5% is about $19,583

- 5% is about $27,975

What This Looks Like in Portland Oregon, Cedars East, Vancouver WA, Brush Prairie Washington, Battle Ground Washington

In Portland Oregon, entry-priced homes can cluster in areas like Foster Powell homes or parts of Northeast Portland real estate. A 3% to 5% down payment can be realistic if you use seller credits to cover closing costs, especially now that inventory has improved and days on market average in the 40s based on recent reports. This is why this matters to you. You can negotiate more strategically.If you’re moving to Portland Oregon but comparing Southwest Washington homes for sale, Vancouver WA homes for sale can sometimes stretch your budget. Battle Ground Washington and Brush Prairie Washington may deliver more yard or newer construction at the same payment compared to some inner Portland neighborhoods. Factor in Washington’s lack of state income tax and Oregon’s lack of sales tax to understand your true monthly and annual costs.

Cedars East is a small pocket that can appeal if you value a quieter feel with proximity to Vancouver. If you’re a tech professional or doctor relocating, convenience to major corridors and hospitals is as important as price. If you need new construction homes in Vancouver WA or prefer established Portland walkable neighborhoods like Sellwood or Alameda, your down payment path might differ. Use the C3 approach to weigh care for your lifestyle, confidence in your payment, and communication with your lender to fine-tune cash to close.

What Most People Get Wrong About Down Payments in Portland Oregon

- You don’t need 20% down. Many first-time buyers succeed with 3% to 5% down or 3.5% FHA. VA is 0% for eligible military families.

- Down payment is not the only upfront cost. Closing costs at 2% to 4% and prepaids matter. Plan for inspections and early repairs too.

- FHA versus conventional is not always about credit. With rates near 6.5%, the monthly difference can swing based on PMI versus MIP and your price range.

- Assistance programs are not just for very low incomes. Many target first-time buyers with moderate incomes and can be stacked with credits.

- Timing the Portland real estate market perfectly is unrealistic. With steady demand from employers and rising inventory, a solid plan beats waiting for a unicorn deal.

Frequently Asked Questions

How much do you need down to buy in Portland Oregon with FHA in 2026?

You need at least 3.5% down with FHA. On a $559,500 Portland home, that’s about $19,583 plus roughly 2% to 4% for closing costs. FHA also has upfront and monthly mortgage insurance that you should factor into your budget.What is the minimum down payment for a conventional first-time buyer in Portland?

Typically 3%. On a $559,500 price, that’s about $16,785. You’ll pay PMI until you reach 20% equity. In some cases, 5% down lowers PMI and may improve monthly affordability compared to 3%.Can you buy in Vancouver WA or Battle Ground Washington with 0% down?

Yes, if you’re eligible for a VA loan. VA offers 0% down and no monthly mortgage insurance. You may still pay a funding fee and standard closing costs, which can sometimes be covered with credits.How much should you budget for closing costs in Portland Oregon?

Plan for 2% to 4% of the purchase price. On $559,500, expect about $11,190 to $22,380. That includes lender fees, title, escrow, taxes, insurance, and prepaid interest. Seller or lender credits can offset part of this.Are there first-time buyer programs that reduce your cash to close in Portland?

Yes. State and local programs can provide down payment or closing cost assistance for eligible buyers. Income limits, purchase price caps, and education requirements may apply. Ask your lender about stacking options with credits.Should you put 20% down to avoid PMI in Portland?

Only if it fits your plan. Avoiding PMI lowers monthly costs, but 20% can slow your timeline and drain reserves. In an active Portland housing market, 5% to 10% down plus a strong emergency fund can be the smarter move.How do taxes differ if you buy in Portland Oregon vs Vancouver WA?

Oregon has no sales tax. Washington has no state income tax. Your take-home pay, spending patterns, and property taxes will affect overall affordability. Compare your full annual budget, not just the mortgage payment.Does a bigger down payment always beat a rate buydown?

Not always. A targeted 2-1 buydown or permanent buydown can reduce early payments more than a small increase in down payment. Run the numbers with your lender to see which option wins for your timeline and goals.What if you want a condo in Sellwood or a home in Irvington?

Condo loans can have extra requirements and HOA dues that affect approval and monthly payment. Single-family homes may allow more flexible financing. Keep your analysis neighborhood specific and property-type aware.Are Portland market trends favorable for first-time buyers in 2026?

Rising inventory and steady demand suggest more choice and negotiation room. With rates around 6.5% and a median near $559,500 per recent reports, a clear down payment and credit strategy can help you compete confidently.The Bottom Line

You can buy a first home in Portland Oregon in 2026 with as little as 3% to 5% down on a conventional loan or 3.5% with FHA, and 0% if you’re VA-eligible. On a $559,500 home, that’s about $17,000 to $28,000 for down payment plus 2% to 4% for closing costs. Your smartest path is neighborhood specific and lender modeled. When you compare total cash to close, monthly payment, and program rules side by side, you’ll choose the option that delivers care for your budget, confidence in your payment, and clear communication at every step.If you’re ready to explore your options for how much down payment you need for a first-time home in Portland Oregon, Cedars East, Vancouver WA, Brush Prairie Washington, or Battle Ground Washington, Lisa Mehlhoff at Real Broker can walk you through the specifics for your situation. With 20 years of experience, 200 closed transactions, and a C3 approach, you get a comprehensive and caring real estate experience. Clients consistently note responsive guidance and neighborhood expertise that make decisions easier.

Important information and disclaimers:

- This content is for educational purposes only and not legal, tax, or financial advice. Loan limits, underwriting, and program guidelines change. Verify all numbers with a licensed lender and your tax professional.

- Equal Housing Opportunity. Real estate brokerage licensed in Oregon.

- Real estate decisions are neighborhood specific. Always confirm property details, HOA rules, and local requirements before making offers.

Lisa Mehlhoff, Real Estate Agent, Real Broker, Oregon License 200603251 Phone: 503.490.4888 Office: 2175 NW Raleigh St, Portland, OR 97210

Testimonials reflect individual experiences and are not guarantees of future outcomes. Buyers like Corey Stafford, Sachi Patel, and Iris Torres have highlighted responsive support, deep Portland housing market knowledge, and guidance tailored to first-time and move-up buyers.

Categories

Recent Posts

"My job is to find and attract mastery-based agents to the office, protect the culture, and make sure everyone is happy! "