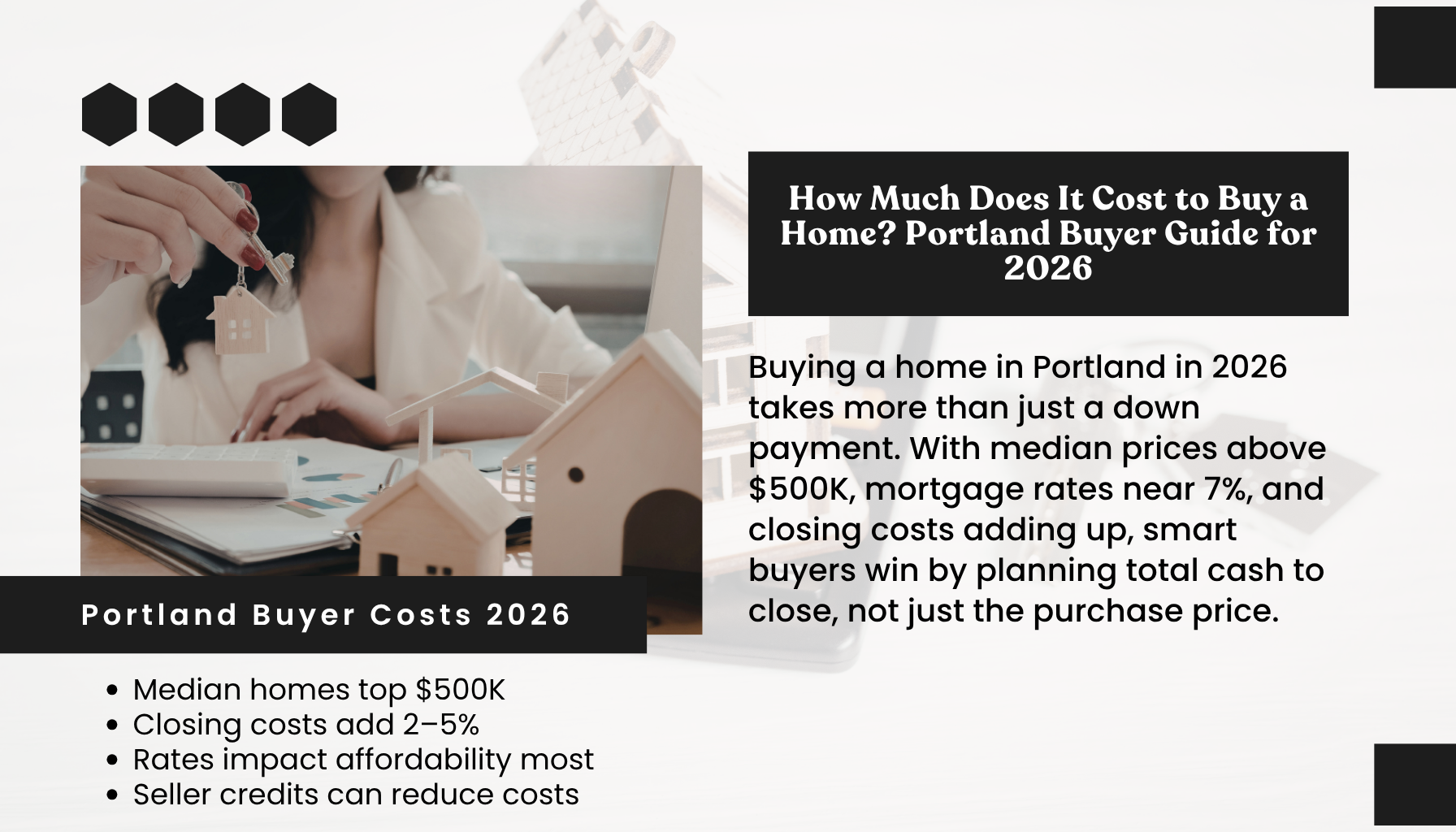

How Much It Costs to Buy a Home in Portland Oregon in 2026

How much does it cost to buy a home in Portland Oregon in 2026?

In Portland, Oregon in 2026, expect total purchase costs of about $515K–$550K for a median home, with 3.5%–5% down, 2%–5% closing costs, and 6.5%–7.0% rates shaping your payment.

Why This Matters Right Now in Portland, Oregon

You are stepping into a balanced Portland market in 2026, which changes how you plan your budget and offers. Inventory sits around a 3.0‑month supply, and market time averages 55 to 80 days, so you have room to negotiate without losing good homes to bidding wars overnight. Median sale prices range from about $507,333 to $525,000, with January listings near $480,000 to $524,251. Around 27.2% of homes still sell over list, but 51.7% close under list and 23.3% see price reductions. With mortgage rates hovering near 6.5% to 7.0%, small changes in price, credits, and rate buydowns can make a big dent in your monthly payment. If you focus on a clear cash‑to‑close plan and smart negotiation, you can secure the right Portland home without stretching beyond comfort.

What You Need to Know Before Buying in Portland, Oregon

You should budget beyond the purchase price. Plan for your down payment plus closing costs. Closing costs typically run 2% to 5% of the price. On a $520,000 home, that is roughly $10,400 to $26,000. With an FHA loan at 3.5% down, your upfront cash target often lands between $28,200 and $44,200 plus prepaid expenses.

Market data shows median sales near $507,333 to $525,000 and a sale‑to‑list price ratio around 0.994. Homes often go pending in 19 to 33 days, which gives you time to verify inspection, appraisal, and insurance without cutting corners. Single‑family homes track toward the higher end, with metro medians reported around $534,000 to $549,000, while townhomes and condos trend lower and offer more negotiation leverage.

Key takeaways for Portland in 2026:

- You can often negotiate price or credits since 51.7% of homes sell under list.

- You face occasional competition, with 27.2% over list, especially in summer.

- Rates near 6.5% to 7.0% shape affordability more than small price swings.

- First‑time buyers commonly use FHA at 3.5% down or local assistance to reduce cash needed.

- Condos typically offer softer pricing and choices, while single‑family homes see tighter competition.

Using Portland’s Balanced Conditions to Your Advantage

When listings show 23.3% price reductions, you can time your offer after a cut and ask for a seller credit toward closing costs or a rate buydown. That can lower your monthly payment more than a small price discount alone.

How to Compare Your Options in Portland, Oregon

Your best strategy is to compare property types and financing paths side by side. Single‑family homes in Portland often sit in the $520,000 to $550,000 band at the median, while many condos and townhomes come in lower. With a 3.5% down FHA loan, your entry point can be more approachable, though you will carry mortgage insurance. Conventional loans with 5% down may reduce long‑term insurance costs if your credit profile is strong.

Look at seasonality. Portland’s summer brings more competition, which raises the chance of paying over list. Winter and early spring often bring softer pricing and more seller flexibility. In 2026, homes typically pend in 19 to 33 days, so you have time to compare two or three homes and their total monthly costs before deciding.

Be sure to weigh rate buydowns and credits. A modest seller credit applied to points can move your payment more than the same dollar amount off the price. With rates near 6.5% to 7.0%, a buydown can be the difference between comfortable and stretched.

Key factors to evaluate:

- Total monthly payment: Principal, interest, taxes, insurance, and HOA if any, not just price.

- Cash to close: Down payment plus 2% to 5% closing costs, minus any seller credits or assistance.

- Resale and maintenance: Single‑family homes may have higher upkeep but broader buyer pools, while condos have HOAs that cover some costs but add monthly dues.

Your Step‑by‑Step Guide to Estimating Cash to Close in Portland, Oregon

1) Set your target price range. Use current Portland medians around $507,333 to $525,000 as a benchmark. If you prefer single‑family homes, expect the metro median near $534,000 to $549,000.

2) Choose a loan type and down payment. Many first‑time buyers use FHA at 3.5% down. Conventional at 5% down can work if your credit is strong and you want to reduce mortgage insurance later.

3) Estimate closing costs at 2% to 5%. On a $520,000 price, budget $10,400 to $26,000. Include lender fees, title and escrow, appraisal, recording, and prepaid taxes and insurance.

4) Factor in rate and payment. At 6.5% to 7.0%, secure a rate quote and consider a temporary or permanent buydown. A small credit applied to points can save more per month than a modest price cut.

5) Add HOA if applicable. Many Portland condos and townhomes have monthly dues that affect qualification and affordability.

6) Plan for inspections and appraisal. Inspection fees and potential repairs can add near‑term costs. Appraisals must support value in a market where 51.7% sell under list.

7) Use negotiation to offset cash. In a 3.0‑month supply market, you can often ask for seller credits, especially after a price reduction or if days on market extend beyond 30.

8) Confirm assistance options. Oregon programs and local grants can help with down payment or closing costs if you meet eligibility rules.

9) Build a move‑in cushion. Budget for utilities, minor repairs, and furnishings so you are not cash tight after closing.

What This Looks Like in Portland, Oregon

Picture a $520,000 Portland purchase. With FHA at 3.5% down, your down payment is $18,200. Closing costs at 3% would be about $15,600, putting cash to close near $33,800 plus prepaid items and any rate buydown. If you negotiate a 2% seller credit, that is $10,400 back to cover closing costs or points, which can ease your upfront and monthly burden.

If you pivot to a $475,000 condo in Portland, the down payment at 3.5% is $16,625 and closing costs at 3% run about $14,250. HOA dues might be $250 to $450 per month, which you should add to your monthly budget. Condos carry softer pricing and higher inventory, so your chance of a seller credit is often better than with a similarly priced single‑family home.

Timing matters. Homes pend in 19 to 33 days, yet average market time can run 55 to 80 days. If a Portland listing sits more than 30 days or shows a price cut, you gain leverage. With 27.2% still selling over list, focus on well‑priced, turnkey options early in the week so you can act quickly without rushing your due diligence.

What Most People Get Wrong About Buying in Portland, Oregon

You might think price is everything, but in 2026 monthly payment and total cash to close carry more impact. With rates near 6.5% to 7.0%, a seller credit used for a rate buydown can reduce your payment more than a small discount on price. Another misconception is assuming every home sparks a bidding war. Portland is balanced now. Since 51.7% of homes close under list and 23.3% show reductions, you can negotiate repairs or credits, especially on properties with longer days on market.

Finally, many first‑time buyers skip condos or townhomes by default. Those segments in Portland often offer better inventory, lower entry prices, and faster paths to ownership, while still giving you resale potential if you choose a well‑located, well‑managed building with strong financials.

Frequently Asked Questions

What is the average price to buy a home in Portland, Oregon in 2026?

Median sales range from about $507,333 to $525,000, with metro single‑family medians near $534,000 to $549,000. Your final price depends on property type and location within Portland. Condos and townhomes usually price lower than single‑family homes.

How much cash do you need upfront to buy in Portland, Oregon?

Plan for 3.5% to 5% down plus 2% to 5% closing costs. On a $520,000 purchase, that is roughly $28,200 to $44,200 or more when you include prepaid taxes and insurance. Seller credits and assistance programs can reduce your cash to close.

Are homes still selling over asking price in Portland, Oregon?

Yes, but less often. About 27.2% sell over list, while 51.7% sell under list. The sale‑to‑list ratio is roughly 0.994. You can often negotiate, especially on homes with longer days on market or recent price reductions.

How long do homes take to sell in Portland, Oregon in 2026?

Homes typically go pending in 19 to 33 days, though overall market time averages 55 to 80 days. Faster pendings are common for well‑priced single‑family homes. Condos and homes with pricing issues tend to sit longer, increasing buyer leverage.

What interest rates should you expect in Portland, Oregon this year?

Forecasts put typical rates in the 6.5% to 7.0% range in 2026. Your exact rate depends on credit, loan type, down payment, and points. A temporary or permanent buydown using seller credits can help lower your monthly payment.

What closing costs should you expect in Portland, Oregon?

Expect 2% to 5% of the purchase price. This includes lender fees, title and escrow, appraisal, recording, and prepaid taxes and insurance. You can often ask the seller to cover part of these costs through a credit, especially on homes with longer market time.

Is an FHA loan a good option for first‑time buyers in Portland, Oregon?

It can be. FHA allows 3.5% down and flexible credit guidelines, which helps keep cash to close manageable. You will have mortgage insurance, so compare it to a 5% down conventional option. In Portland’s balanced market, you can sometimes offset costs with credits.

Are condos a smart first step in Portland, Oregon?

Often yes. Condos typically come in below single‑family prices and offer more inventory. You should compare HOA dues and building reserves, but condos can provide an affordable, turn‑key entry into Portland ownership with solid resale if well located.

When is the best time to buy in Portland, Oregon in 2026?

Late fall and winter often bring less competition and more seller flexibility, which can mean better pricing or credits. Spring and summer see more listings but also more bidding pressure. Your schedule and financing readiness should guide timing.

What negotiation strategies work in Portland, Oregon right now?

Target homes with 20 to 30 days on market or recent price cuts, ask for credits toward closing costs or a rate buydown, and keep your inspection focused on safety or major systems. In a 3.0‑month supply market, balanced offers often win without overpaying.

The Bottom Line

In Portland, Oregon in 2026, you should plan for a median purchase around $507,333 to $525,000, with total cash to close typically landing in the $515,000 to $550,000 all‑in range when you include down payment and closing costs. Rates near 6.5% to 7.0% make payment strategy as important as price. Use the city’s balanced conditions to negotiate credits and consider condos or townhomes if you want a lower entry point. With a clear budget, a strong pre‑approval, and a focus on total monthly cost, you can buy confidently in Portland this year.

If you're ready to explore your options for how much it costs to buy a home in portland, oregon, Lisa Mehlhoff at Lisa Mehlhof Homes can walk you through the specifics for your situation.

503-490-4888 2175 NW Raleigh St, Portland, OR, 97210 220603251

503-490-4888 2175 NW Raleigh St, Portland, OR, 97210 220603251

Categories

Recent Posts

"My job is to find and attract mastery-based agents to the office, protect the culture, and make sure everyone is happy! "