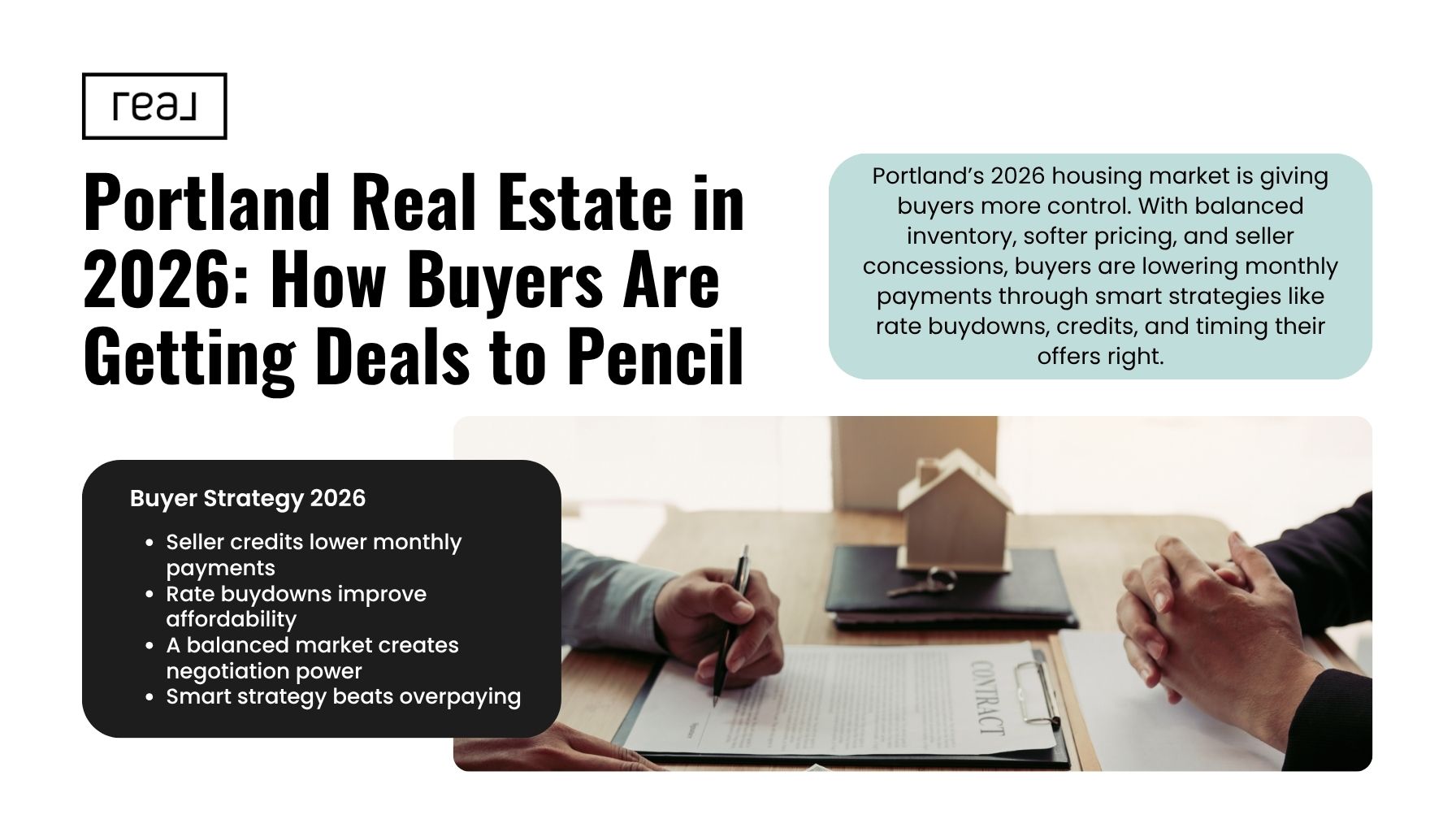

Interest Rates in 2026: How Portland Buyers Are Actually Getting Deals to Pencil

TLDR

- Balanced inventory near 3.6 months plus modest price dips creates buyer leverage.

- Conforming rates around 6 percent pair with seller credits and buydowns.

- Strategy stack: pre-approval, rate buydown, inspection credits, targeted neighborhoods.

- Portland Metro median near $498K with 42 days on market helps negotiations.

What does “getting a deal to pencil” in 2026 really mean?

When buyers tell me a home needs to pencil, they want the monthly payment, upfront costs, and longer term equity story to make sense. In early 2026 our Portland Metro market is balanced, with roughly 3.6 months of inventory and a median sale price near $498,000. That combination puts real negotiating tools back in play. Days on market are hovering around the low 40s, which gives you time to conduct due diligence without losing the house overnight. These numbers come from our regional multiple listing service and align with what I see in weekly previews and offers across the metro.

Prices are slightly lower year over year, about 2.5 percent down. Buyers who plan carefully can convert that modest decline into larger effective savings by adding a rate buydown, asking for repair credits, and timing their offer around price reductions. As a Portland Oregon Real Estate Agent based in the city, I’m seeing that stack translate into meaningful monthly differences.

Here is how I define it as Lisa Mehlhoff:

- Your payment target and cash-to-close fit within your comfort zone.

- You negotiate credits or pricing that offset today’s interest rate.

- You choose a neighborhood with a clear resale story and lifestyle fit.

How do interest rates and concessions work in Portland right now?

Conforming 30-year fixed rates have hovered close to 6 percent in early 2026, per national series tracked by the Federal Reserve’s FRED dataset. You can review the trend line here: 30-Year Fixed Mortgage Rate Series. Lenders across Portland and Clark County are quoting similar ranges for well-qualified buyers, and some portfolio programs sit slightly below or above depending on credit and down payment.

The key is that this rate environment coincides with a balanced Portland market. Local MLS data since late 2025 shows a meaningful list-to-sale spread, with many homes closing under asking and average discounts often in the 6 to 7 percent range. That discount can fund a permanent rate buydown, your closing costs, or targeted repairs. Statewide context from the Oregon REALTORS market data page and the FHFA House Price Index supports the picture of slowed price growth and more buyer options compared to the frenzy years.

What is a temporary buydown vs a permanent buydown?

- Temporary buydown: The seller pays points to reduce your rate for the first one to two years. A 2-1 buydown typically lowers year one by 2 percentage points and year two by 1. The cost often equals the interest differential for those periods, commonly around 1.5 to 2.5 percent of the loan amount.

- Permanent buydown: You or the seller pay discount points to reduce your note rate for the life of the loan. One point equals 1 percent of the loan amount and can cut the rate about 0.25 to 0.375. I often negotiate a seller credit of 1 to 2 percent that buyers then allocate to a permanent buydown.

Where are Portland buyers actually making the numbers work?

This year I’m guiding clients toward submarkets where pricing, commute patterns, and community amenities support both livability and strong resale. It is not about chasing the absolute lowest price. It is about buying at a market-appropriate price with room to negotiate and a plan to optimize financing.

- SW Portland: Hillsdale and Multnomah Village

- East Vancouver Washington Real Estate: East Vancouver neighborhoods near Fourth Plain and the Cedars area have attracted first-time buyers and investors after notable price softening in 2025. Median pricing around the low 400s has pulled in new demand.

- Lake Oswego Oregon Real Estate Market: Premium schools, lake lifestyle, and strong retail. Prices run higher, but condos and townhomes create entry points for relocating professionals.

- East Vancouver Washington Real Estate beyond Cedars: Suburban convenience with I-205 access and new construction in pockets. Family buyers appreciate the parks and newer floor plans.

Portland’s demographic and employment base remains solid, with strong educational attainment and a metro population around 2.6 million per the city’s housing analysis. See the city’s long-range housing needs context at Portland Housing Needs Analysis. For Clark County trends that influence East Vancouver and Brush Prairie, the Washington OFM monthly economic report is a reliable resource.

What are the pros and cons of buying with rates near 6 percent?

Pros:

- Negotiation power. Balanced supply near 3.6 months plus longer days on market opens room for credits.

- Flexible financing playbook. Seller-paid buydowns and closing costs can offset rate headwinds.

- More choice. Inventory is higher than 2021 peaks, which lets you be selective on location and condition.

Cons:

- Monthly payment sensitivity. Even small rate swings change affordability bands by tens of thousands.

- Tight entry-level segment. SW Portland Oregon homes for sale under $500,000 can still draw multiple offers.

- Uncertain timing. Waiting for a big rate drop is speculative, and prices may rebound faster than rates fall.

How do I stack strategies so the math pencils month one and year five?

Think in layers. Your first layer is a thorough pre-approval that models multiple rate paths and payment buffers. I encourage clients to price in a 0.25 percent rate cushion so there are no last-minute surprises. Your second layer is the negotiation plan. Ask for a seller credit equal to 1 to 2 percent of the price, earmarked for a permanent buydown or closing costs. Your third layer is inspection strategy. Focus on high-impact safety and system items, then convert non-critical asks into a closing credit.

One of my clients, a tech professional relocating to the westside, targeted a townhome just inside Portland city limits for walkability. We negotiated a 1.75 percent seller credit that bought the rate down by 0.375, plus a $2,000 credit for electrical panel work. Total impact was roughly $235 per month lower than the initial quote. That turned a nice unit into a strong hold with commuting access to Hillsboro via Highway 26.

Another client, a physician moving to be near OHSU, used a physician-loan program with 5 percent down and no PMI. In Lake Oswego, we found a condo with excellent reserves. The seller covered one point to permanently buy down the rate, and we timed closing to align with a rate float-down at no extra cost. Payment landed inside the hospital’s housing stipend, which made the relocation friction-free.

For VA-eligible buyers, a zero-down structure can still pencil beautifully when combined with closing cost credits. Military families shopping near East Vancouver and the C-TRAN network often win by targeting well-maintained homes that need only cosmetic refreshes. Ask for enough credit to cover VA non-allowable fees and a small buydown so the first-year budget breathes.

Cost guide for planning:

- Permanent buydown: 1 point equals 1 percent of loan amount, often reduces rate 0.25 to 0.375.

- Temporary 2-1 buydown: around 1.5 to 2.5 percent of the loan amount funded by the seller.

- Typical inspection credit ask: 1 to 2 percent for roof tune-ups, panel updates, GFCI, and sewer scope findings.

- Closing timeline: 30 to 40 days standard, 21 to 25 days possible with a fully underwritten pre-approval.

FAQs

1) Should I wait for rates to drop before buying in Portland? Waiting can be risky. If rates drop meaningfully, demand can spike and erode today’s price and concession advantages. Right now, a balanced market plus credits and buydowns can create an effective rate lower than the headline. If you find the right home and can negotiate a 1 to 2 percent credit, that often beats trying to time the market.

2) How much below list price can I realistically expect? Local MLS data indicates many homes are selling under list, often in the 6 to 7 percent average discount range. The spread varies by ZIP, condition, and price band. Entry-level homes under $500,000 can still see multiple offers in SW Portland, while higher tiers often show more flexibility. We will analyze list-to-sale ratios by neighborhood before you write.

3) Are 2-1 buydowns better than permanent buydowns? It depends on your time horizon. If you plan to refinance or move within two to three years, a seller-paid 2-1 can meaningfully reduce initial payments. If you expect to hold the home longer, a permanent buydown funded by the seller can be more valuable. I model both with your lender so you can compare savings at months 1, 24, and 84.

4) What neighborhoods give the best balance of price and commute? For quick downtown access and schools, Hillsdale and Multnomah Village are great. For affordability and freeway connectivity, East Vancouver Washington Real Estate in Cedars and nearby corridors offers strong value. If you want premium schools with a condo entry point, Lake Oswego works well. We will weigh commute time, amenities, and resale risk for each option.

5) I’m a first-time buyer with limited cash. Can I still negotiate credits? Yes. In a balanced market, sellers often prefer a clean credit for closing costs or rate buydown instead of managing repairs. A 1 to 2 percent credit can cover your lender fees and buy down your rate. We focus inspection asks on safety and system essentials, then convert the rest to a credit to keep timelines on track.

6) How are Clark County trends affecting East Vancouver and Brush Prairie? Clark County shows steady population and employment growth in logistics and healthcare. Washington OFM’s monthly economic report details regional conditions that support demand along the I-5 and I-205 corridors. Price softening in 2025 brought more buyers back, especially around the low 400s. This year I’m still seeing room to negotiate credits in Cedars East Vancouver WA Real Estate.

7) How does the wider economy impact prices here? Home values correlate with jobs, incomes, and lending costs. The FHFA House Price Index shows state-level moderation after pandemic surges. Locally, balanced inventory and steadier days on market have restored a healthier negotiation process. If the national rate trend drifts lower, Portland’s seasonal upswing could firm prices, which is why credits and buydowns matter today.

Conclusion

The bottom line A deal pencils in 2026 when you control the levers that truly move monthly cost. In Portland that means pairing a balanced market with smart concessions. Use a fully underwritten pre-approval, target neighborhoods with durable demand, and negotiate a 1 to 2 percent seller credit devoted to a permanent or temporary buydown. Combine that with focused inspection credits for safety and system items, and your effective payment often lands below the headline rate. If you want a local plan tailored to SW Portland Oregon homes for sale, East Vancouver Washington Real Estate, or the Lake Oswego Oregon Real Estate Market, I’m here to help run the numbers.

Lisa Mehlhof Homes | License #220603251 Call or text 503-490-4888 https://lisamehlhoffhomes-

Categories

Recent Posts

"My job is to find and attract mastery-based agents to the office, protect the culture, and make sure everyone is happy! "