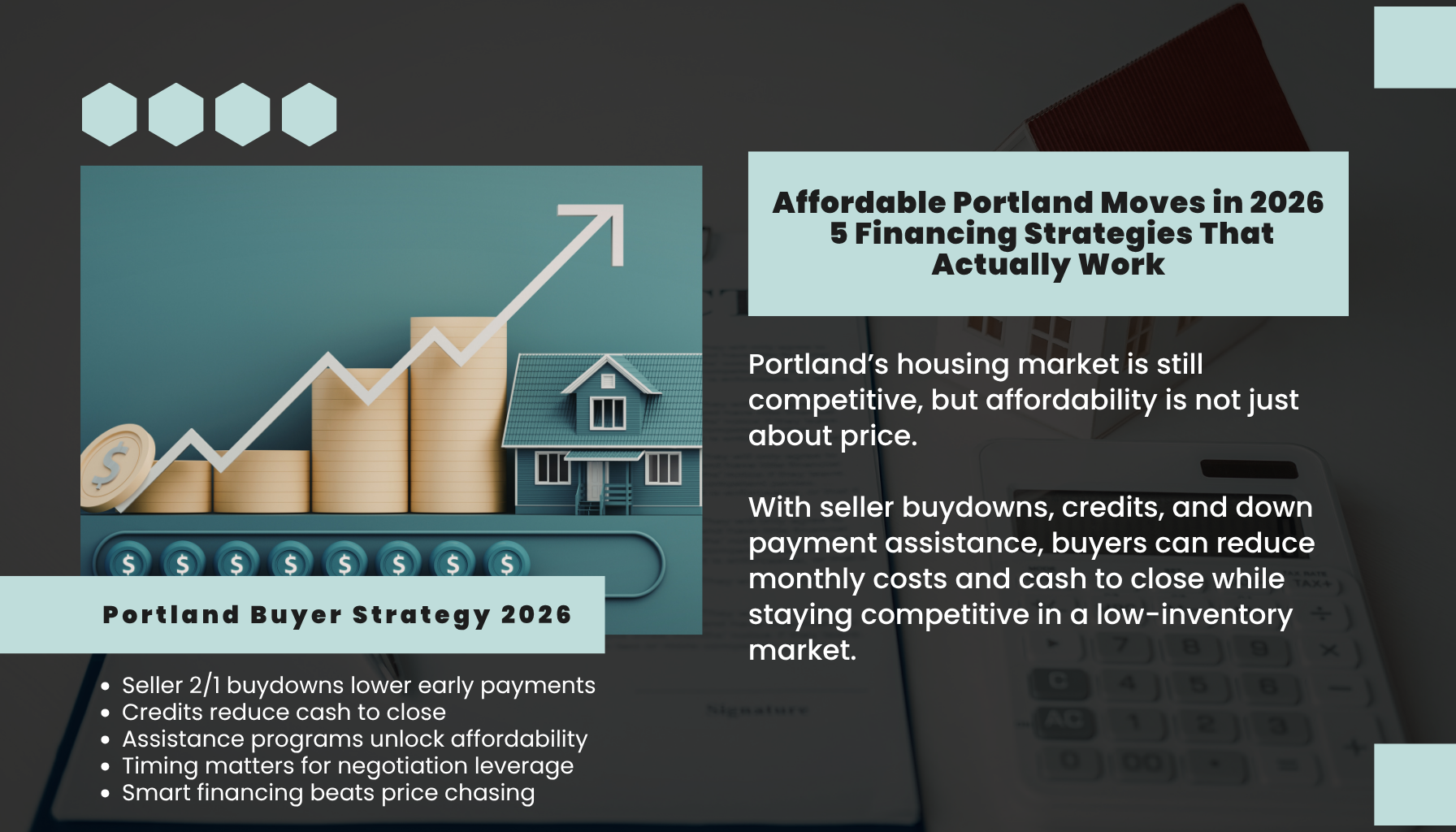

Seller Buydowns, Credits, and Creative Financing: 5 Ways to Make Your Portland Move Affordable

TLDR

- Use seller-paid 2/1 buydowns to reduce payments while rates normalize.

- Combine closing credits with assistance programs to lower cash to close.

- Target neighborhoods where days on market allow stronger buyer negotiation.

- Stack incentives legally and strategically with a Portland Oregon Real Estate Agent.

What do seller buydowns, credits, and creative financing really mean today?

If Portland’s tight inventory has you discouraged, there are still practical ways to make the math work. With about 1.8 months of supply across the Portland metro as of December 2025, buyers must be intentional. That is where seller buydowns, credits, and a few creative playbooks come in. These tools do not cut corners. They align the financing structure, the home choice, and current incentives so your total monthly and upfront costs stay manageable.

The five strategies I guide clients through most often are: temporary rate buydowns funded by sellers, negotiated seller credits to cover closing costs, city or state down payment assistance, targeted Washington programs like House Key Opportunity, and shared-equity models that trade a slice of future appreciation for lower cash today. Each option has rules, timelines, and local nuances that matter across SW Portland, Lake Oswego, the Cedars in East Vancouver, Brush Prairie, and Battle Ground.

Here is how I define it as Lisa Mehlhoff:

- Seller buydown: a seller-funded credit that pre-pays interest to reduce your rate for one to three years.

- Seller credit: funds from the seller to cover your closing costs within program caps.

- Creative financing: legal, layered solutions like assistance grants or shared equity to bridge affordability.

How do these strategies work in Portland and nearby Clark County?

Our market rewards preparation. Portland’s median sale price reached about $572,000 in December 2025, up 6.3 percent year over year, while Southwest Portland premium areas such as Hillsdale and Multnomah Village hovered near $710,000. East Vancouver and the Cedars came in around $530,000, and Brush Prairie and Battle Ground around $520,000 according to recent MLS and county data. Median days on market remain brisk at 13 in Portland, 15 in East Vancouver, and 18 in the exurbs. That means buyers can win, but offers must be tight and strategic.

Inventory sits near 1.8 months in Portland and about 2.0 months across East Clark County, with southern exurbs closer to 2.5 months. A balanced market is typically around six months, as noted by national Realtor research. The takeaway is simple. In seller-leaning conditions, the right concession is more likely when a listing has been active longer than the median for that neighborhood and price point, or when the home needs updates. I track this daily through the Portland Regional MLS and local pricing reports so we can time requests realistically.

Why strategy matters in a 1.8-month market

- A 2/1 buydown can lower your first-year rate by about 2 percent, second year by 1 percent, then revert to the note rate. Seller cost is often 2 to 3 percent of the loan amount.

- Seller credits of 2 to 3 percent are common when the home has been on market beyond local medians, or when the seller values speed and certainty.

- Investor purchases are about 18 percent in Portland and 12 percent in Clark County per CoreLogic Insights. Owner-occupant offers with clean terms plus targeted concessions are competitive in that mix.

Sources: Portland Regional MLS, CoreLogic Insights, Clark County Assessor

Which neighborhoods offer the best fit for each budget and program?

Not all submarkets behave the same. I match strategy to neighborhood tempo, price bracket, and property type.

- Multnomah Village and Hillsdale (SW Portland)

- Details: Walk-to-coffee streets, strong community vibe, convenient TriMet access, mix of mid-century and updated homes. - Watchouts: Older systems can trigger inspection credits. Seismic and sewer scope often matter in due diligence. - Typical timeline: 21 to 30 days when priced right. Credits are most likely on listings lingering past the 13-day city median.

- The Cedars and East Vancouver

- Details: Craftsman-era pockets and established streets, easy access to I-205, parks along the Columbia, and solid schools in Vancouver SD 37. - Watchouts: HOA rules in some subdivisions may restrict exterior updates. Budget for reserves if planning improvements. - Entry-level path: A seller credit paired with Washington’s House Key Opportunity can significantly lower out-of-pocket costs.

- Brush Prairie and Battle Ground

- Details: Newer subdivisions, larger lots, strong school options with Ridgefield and Battle Ground districts, owner-occupancy above 75 percent. - Watchouts: Primarily car-dependent. Understand commute via I-5 and SR 502. Appraisal gaps can surface in rapidly appreciating pockets. - Typical timeline: 25 to 35 days in some tracts, which opens room for 2/1 buydowns or 3 percent closing credits.

- Lake Oswego and First Addition

- Details: Premium proximity to the lake, shops, and schools. The Lake Oswego Oregon Real Estate Market attracts move-up buyers and relocating professionals. - Watchouts: Competitive price points reduce concession odds. Leverage pre-inspections and appraisal strategies. - Entry-level path: Consider condos or townhomes near Kruse Way. HOA dues are higher, but maintenance is lower. Ask for targeted rate buydown instead of price cut.

If you are searching for SW Portland Oregon homes for sale, or reviewing Cedars East Vancouver WA Real Estate, your approach changes by block, not just by ZIP. I use on-the-ground data, plus Travel Portland neighborhood guides, to help you calibrate requests that sellers actually accept.

What are the pros and cons of these five approaches?

Pros:

- 2/1 buydown reduces the payment shock during year one and two while rates evolve.

- Seller credits lower cash to close, which preserves your emergency fund or remodel budget.

- Grants and shared equity reduce the barrier to entry without raising purchase price.

Cons:

- Temporary buydowns do not change the note rate, so plan for year three.

- Program caps apply. FHA, VA, and conventional loans limit total seller contributions.

- Shared-equity models trade part of future appreciation, which impacts long-term upside.

How do I implement the five strategies step by step?

Start with financing structure. I align you with a local lender skilled at temporary buydowns and program stacking. For many buyers, a 2/1 buydown costs the seller roughly 2 to 3 percent of the loan amount. We weigh that against a price reduction. If interest rates ease later, you may refinance. If not, you have still banked two years of lower payments.

Next, we negotiate credits. FHA typically permits up to 6 percent of the price in seller concessions, conventional typically allows 3 percent with low down payments and up to 6 percent at 10 to 25 percent down, and VA allows most closing costs plus concessions up to 4 percent. I structure offers within those caps. In Clark County, I often combine credits with the Washington State Housing Finance Commission House Key Opportunity program to offset closing costs.

We also look at grants. The Portland Housing Bureau has offered down-payment assistance in the $20,000 to $35,000 range. Timing matters, so I monitor application windows. In Washington, House Key and related programs offer reduced-rate or deferred assistance loans that pair cleanly with seller credits. If energy efficiency is your priority, the Energy Trust of Oregon provides rebates that can stretch your post-close budget.

One of my clients, a tech couple moving from California, targeted a Hillsdale home around $900,000. We secured a 2/1 buydown funded by a 2.5 percent seller credit. That reduced their first-year payment by several hundred dollars, then they refinanced during a seasonal dip. The cash they saved at closing went directly into triple-pane windows and a heat pump.

Another client, a first-time buyer focused on Cedars East Vancouver WA Real Estate, layered a modest seller credit with House Key Opportunity. Their out-of-pocket closing costs dropped by almost 60 percent. We timed the offer after day 20 on market, which aligned with the seller’s price expectations and our credit request. They moved in with reserves intact.

For data-driven timing, I watch the first 14 days of each listing. In sub-$600,000 segments, well-priced homes often see eight or more showings per week. If activity lags, sellers become more open to buydowns or credits. I verify these trends through Portland Regional MLS stats, then calibrate our offer.

If you are relocating for OHSU or Legacy, I target SW corridors with reliable commutes. If you are monitoring East Vancouver Washington Real Estate, we focus on days-on-market trends near the I-205 corridor. Either way, I handle the sequencing so you do not overpay upfront or monthly.

FAQs

1) How much does a 2/1 buydown usually cost and who pays it? A typical 2/1 buydown costs about 2 to 3 percent of the loan amount. The seller funds it as a closing credit to prepay the rate reduction. Year one is about 2 percent below the note rate, year two is about 1 percent below, then it reverts. We compare this cost to a price cut and choose the option that best protects cash flow and appraisal.

2) Can I combine seller credits with down payment assistance in Portland or Vancouver? Yes, in many cases. For example, you can combine a seller credit with Portland Housing Bureau assistance or the WSHFC House Key Opportunity program. The key is staying within program and loan guidelines for total concessions. I coordinate with your lender to stack benefits without exceeding caps or triggering underwriting issues.

3) Are condos better or worse for negotiating concessions? Condos can be great candidates because HOA dues increase monthly costs. Sellers often recognize the impact and may be open to a buydown or closing credit. Underwriting can be slightly tighter and rates sometimes run 40 basis points higher. I review HOA budgets, litigation status, and special assessments. If risks are elevated, I push for a stronger credit or price adjustment.

4) What if rates drop after I buy with a 2/1 buydown? If rates decline, refinancing can lock in a permanent lower rate. You still benefited from lower payments during the initial two years, which improves cash flow while you settle in. If rates do not drop, plan for the payment at your note rate in year three. I use lender scenarios to ensure you are comfortable at all phases before we write the offer.

5) How do I know where concessions are realistic in SW Portland or Clark County? I look for days on market that exceed local medians. Portland’s median sits around 13 days, East Vancouver about 15, and Brush Prairie or Battle Ground near 18. When a listing passes those thresholds, sellers are more receptive. I also weigh condition, seasonality, and competition from investors. These signals, confirmed through Portland Regional MLS, guide our ask.

6) Can I assume a low-rate VA loan on a Portland or Vancouver property? Sometimes. VA loans are often assumable with lender and servicer approval, and qualifications still apply. You must confirm whether the seller’s entitlement will be restored or remain tied up. Timelines depend on servicer responsiveness. While not one of the five strategies above, VA assumptions can be powerful for Military Families when the numbers and terms align.

Conclusion

The bottom line Affordability is not just about price. It is about crafting the right structure for your life and your monthly budget. In a market running at 1.8 to 2.5 months of supply, smart buyers use tools like buydowns, credits, and assistance programs to compete without overextending. Whether you are exploring SW Portland Oregon homes for sale, comparing the Lake Oswego Oregon Real Estate Market, or focusing on East Vancouver Washington Real Estate, I will help you stack the right options. Let us build a plan that protects your cash, secures the home, and sets you up to thrive in year one and beyond.

Lisa Mehlhof Homes | License #220603251 Call or text 503-490-4888 https://lisamehlhoffhomes-

Categories

Recent Posts

"My job is to find and attract mastery-based agents to the office, protect the culture, and make sure everyone is happy! "